MER EMI (Monthly Equal Repayment Equated Monthly Installment) is a financing option that allows credit cardholders to convert their large purchases or outstanding credit card balance into manageable monthly installments. This feature helps ease the repayment burden by breaking down high-value transactions into smaller, fixed payments spread over a specified period.

Importance of MER EMI

The MER EMI option is particularly significant for credit card users who wish to:

- Manage High-Value Purchases: Spread the cost of expensive items over time.

- Maintain Cash Flow: Prevent immediate cash outflows and budget effectively.

- Avoid High Interest: Pay a structured interest rate instead of high revolving credit card interest rates.

About HDFC Credit Card

HDFC Bank is one of India’s leading private sector banks, offering a variety of credit cards tailored to different customer needs. The HDFC Credit Card MER EMI option provides cardholders with flexibility and convenience, making it easier to manage their finances without incurring high interest rates typical of unpaid credit card balances.

This guide aims to provide an in-depth understanding of MER EMI on HDFC credit cards, covering everything from how it works to its benefits, eligibility, application process, and management strategies.

Understanding MER EMI on HDFC Credit Card

What is MER EMI?

MER EMI (Monthly Equal Repayment Equated Monthly Installment) on HDFC credit cards is a feature that allows cardholders to convert their high-value purchases or total outstanding balance into monthly installments. This feature helps cardholders manage their finances by offering a fixed repayment schedule at a lower interest rate compared to the standard credit card interest.

How MER EMI Works

- Conversion of Purchases: Eligible purchases above a certain amount can be converted into EMIs at the time of transaction or within a specified period after the purchase.

- Tenure Options: Cardholders can choose from various tenure options (e.g., 3, 6, 9, 12, 24 months) based on their convenience and financial planning.

- Fixed Monthly Payments: The total amount, including interest, is divided into equal monthly installments.

- Interest Rate: A predetermined interest rate is applied to the EMI, which is generally lower than the standard credit card interest rate.

Benefits of MER EMI on HDFC Credit Card

- Manageable Payments: Large expenses are spread out over time, reducing financial strain.

- Lower Interest Rates: Compared to revolving credit, MER EMI offers reduced interest rates.

- No Credit Card Overdrafts: Prevents exceeding credit limits and additional charges.

- Improved Budgeting: Helps in better financial planning and cash flow management.

Common Uses of MER EMI

- High-Value Purchases: Electronics, furniture, travel, or jewelry.

- Emergency Expenses: Medical bills or urgent repairs.

- Balance Conversion: Converting the total outstanding balance to EMIs to avoid high interest rates.

Eligibility and Terms for MER EMI

Eligibility Criteria

- Credit Card Type: Not all credit cards may be eligible; specific cards offered by HDFC have this feature.

- Transaction Amount: Minimum transaction amount required to convert to EMI (e.g., ₹2,500 or above).

- Credit History: Good repayment history may be required for eligibility.

- Cardholder Status: Active cardholders in good standing with no overdue payments.

Terms and Conditions

- Processing Fee: A one-time fee may be charged for setting up the EMI plan.

- Interest Rate: Varies based on the tenure and type of transaction. Typically lower than regular credit card interest rates.

- Foreclosure Charges: A penalty may be charged for early repayment or foreclosure of the EMI plan.

- Default: Failure to pay EMIs on time can result in penalties and affect credit score.

Example Scenarios

- Scenario 1: Ms. Sharma purchases a television for ₹60,000. She converts it into a 12-month EMI plan at an interest rate of 12% per annum.

- Scenario 2: Mr. Rao faces a sudden medical emergency with a bill of ₹1,00,000. He uses his HDFC credit card and converts the bill into a 6-month EMI plan to manage payments better.

How to Apply for MER EMI on HDFC Credit Card

Application Process

At the Time of Purchase:

- Select EMI Option: While making an eligible purchase, choose the EMI option if available at the merchant’s payment gateway.

- Select Tenure: Choose the desired tenure for the EMI plan.

- Confirm: Complete the transaction, and the purchase will be converted into EMIs.

Post Purchase:

- Log into NetBanking: Access the HDFC Bank NetBanking portal.

- Navigate to Credit Card Section: Find the ‘Credit Card’ section and select ‘Transact’ or ‘Offers.’

- Select EMI Option: Choose the ‘Convert to EMI’ option for eligible transactions.

- Choose Tenure: Select the preferred tenure for the EMI plan.

- Confirm: Complete the process to convert the transaction into EMIs.

Via Customer Service

- Call Customer Service: Contact HDFC Bank’s credit card customer service.

- Request EMI Conversion: Request to convert eligible transactions into EMIs.

- Provide Details: Provide necessary details and confirm the tenure and interest rate.

- Confirmation: Receive confirmation of the conversion and the EMI schedule.

Via Mobile App

- Open HDFC Mobile Banking App: Access your account through the HDFC mobile banking app.

- Go to Credit Card Section: Navigate to the ‘Credit Card’ section.

- Choose EMI Option: Select the option to convert transactions to EMI.

- Select Tenure: Pick the tenure for the EMI plan.

- Confirm: Confirm the conversion and EMI details.

Important Considerations

- Eligibility of Transactions: Not all transactions may be eligible for conversion.

- Processing Time: The conversion process may take a few business days.

- Interest and Fees: Understand the interest rate and any additional fees before confirming the EMI conversion.

Interest Rates and Fees

Understanding Interest Rates

- Annual Percentage Rate (APR): The annual rate charged for borrowing, represented as a percentage of the principal.

- Monthly Interest Rate: The interest rate applied monthly to calculate the EMI.

Current Interest Rates for MER EMI

| Tenure | Interest Rate |

|---|---|

| 3 Months | 1.25% per month |

| 6 Months | 1.20% per month |

| 9 Months | 1.15% per month |

| 12 Months | 1.10% per month |

| 24 Months | 1.05% per month |

Note: Interest rates are indicative and may vary based on HDFC Bank’s policies and promotions.

Processing Fees

- Percentage of Transaction: Typically ranges between 1% to 2% of the transaction amount.

- Minimum Amount: A minimum fee may apply regardless of the transaction amount.

Foreclosure Charges

- Percentage of Outstanding Balance: Usually 2% to 3% of the remaining balance if the EMI plan is closed early.

- Flat Fee: Some plans may have a flat fee for foreclosure.

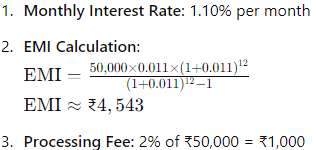

Example Calculation

For a purchase of ₹50,000 converted to a 12-month EMI plan at 1.10% per month:

Total payable over 12 months would include the processing fee and interest on the principal.

Managing MER EMI Effectively

Setting Up Automatic Payments

- Ensure Timely Payments: Avoid missed EMIs by setting up automatic payments through NetBanking or mobile app.

- Prevent Penalties: Timely payments prevent penalties and protect your credit score.

Monitoring Transactions

- Regular Statements: Review credit card statements to track EMI payments and remaining balance.

- NetBanking/Mobile App: Use online tools to monitor and manage EMI transactions.

Budgeting for EMIs

- Allocate Monthly Funds: Include EMI payments in your monthly budget to ensure funds are available.

- Adjust Spending: Reduce discretionary spending to accommodate EMI payments without financial stress.

Early Repayment Strategies

- Lump-Sum Payments: Use bonuses or savings to make lump-sum payments towards the EMI balance.

- Partial Prepayments: Make partial payments to reduce the principal and interest burden.

Dealing with Financial Difficulties

- Contact HDFC: If facing financial difficulties, contact HDFC Bank for possible solutions such as restructuring the EMI plan.

- Consider Rescheduling: Explore options to extend the tenure or lower the EMI amount temporarily.

Advantages of Regular Review

- Stay Informed: Regularly review your EMI plan to stay informed about the outstanding balance and interest paid.

- Refinance if Necessary: If better interest rates or terms become available, consider refinancing the EMI plan.

Alternatives to MER EMI

Revolving Credit

- Pros: Flexibility in payment amounts.

- Cons: Higher interest rates and potential for accruing significant debt.

Personal Loans

- Pros: Often lower interest rates compared to credit card interest.

- Cons: Requires a separate application and approval process.

Balance Transfer

- Pros: Transfer outstanding balance to another card with lower interest.

- Cons: Balance transfer fees and possible limited tenure.

Zero Interest EMI Options

- Pros: No interest charged; only principal amount repaid.

- Cons: May have higher processing fees or limited to specific merchants.

FAQs About MER EMI on HDFC Credit Card

What Transactions are Eligible for MER EMI?

Eligible transactions usually include purchases above a minimum amount (e.g., ₹2,500). Check HDFC’s terms for specific eligibility criteria.

Can I Cancel or Modify the EMI Plan?

Cancellation: Possible within a specified period. May incur a cancellation fee.

Modification: Generally not allowed once set up, but you can prepay or foreclose the EMI plan.

What Happens if I Miss an EMI Payment?

Penalties: Late fees and penalties may apply.

Credit Impact: Missing EMI payments can negatively affect your credit score.

How Do I Know the Applicable Interest Rate?

Check at the Time of Conversion: Interest rates are displayed during the conversion process.

Customer Service: Contact HDFC customer service for current interest rates.

Can I Convert All Types of Purchases to EMI?

Eligibility Varies: Typically high-value retail purchases are eligible. Cash withdrawals or certain types of transactions may not qualify.

Is There a Limit to the Number of EMI Plans I Can Have?

Depends on Credit Limit: As long as you stay within your available credit limit, multiple EMI plans can be set up.

Are Processing Fees Refundable?

Generally Non-Refundable: Once charged, processing fees are typically non-refundable, even if you cancel the EMI plan.

How Does Early Repayment Affect My EMI Plan?

Foreclosure Fee: Early repayment usually incurs a foreclosure fee.

Interest Savings: Early repayment can save on interest costs if done strategically.

What Happens if I Foreclose the EMI Plan?

Foreclosure Charges: A fee is typically charged for closing the EMI plan early.

Final Settlement: Outstanding principal and interest must be settled at the time of foreclosure.

Can I Use Reward Points to Pay EMIs?

Not Directly: Reward points cannot be used to pay EMIs directly but can be redeemed for other benefits that may free up funds for EMI payments.

What Documentation is Required for Applying?

Minimal Documentation: Usually, no additional documentation is needed beyond your HDFC credit card details and NetBanking access.

How Do I Calculate My EMI?

Use EMI Calculator: HDFC’s website or mobile app provides an EMI calculator for accurate estimation.

Manual Calculation: Follow the standard EMI formula for manual calculation.

Are There Promotional Offers on MER EMI?

Check Regularly: HDFC may offer promotional interest rates or fee waivers during certain periods. Check regularly for offers.

Can I Convert Outstanding Balance to EMI?

Yes: Outstanding balances can be converted into EMIs, subject to eligibility and terms.

How Does MER EMI Affect My Credit Limit?

Reduced Limit: The amount converted to EMI reduces your available credit limit until the EMIs are repaid.

What is the Tenure for MER EMI?

Varies by Plan: Tenure options typically range from 3 months to 24 months, depending on the transaction and eligibility.

How is the Interest Rate Determined?

Based on Factors: Interest rates are based on factors like the transaction amount, tenure, and promotional offers.

Can I Convert Multiple Transactions to EMI?

Yes: Multiple eligible transactions can be converted into separate EMI plans as long as the total does not exceed your credit limit.

Are There Any Hidden Charges?

Transparent Fees: HDFC discloses all applicable fees and charges during the EMI setup. Review terms carefully to avoid surprises.

How Does MER EMI Affect My Credit Score?

Positive Impact: Regular EMI payments can positively impact your credit score by demonstrating creditworthiness.

Can I Pay More Than the EMI Amount?

Yes: Paying more than the EMI amount can reduce the principal balance and interest burden.

What is the Process for Early Foreclosure?

Contact Customer Service: Reach out to HDFC customer service to initiate the foreclosure process and understand the charges.

Is the EMI Amount Fixed for the Entire Tenure?

Fixed Amount: The EMI amount remains fixed throughout the tenure, making budgeting easier.

What Happens if I Exceed My Credit Limit?

Fees and Penalties: Exceeding your credit limit can result in over-limit fees and may affect your ability to convert transactions to EMI.

Can I Use the EMI Option for Online Purchases?

Yes: Many online merchants offer the option to convert purchases to EMI at checkout, provided the transaction meets HDFC’s criteria.

Conclusion

Managing finances effectively is crucial in today’s fast-paced world, and MER EMI on HDFC credit cards offers a flexible and convenient way to handle high-value purchases or outstanding balances. By understanding the mechanics, eligibility criteria, interest rates, fees, and effective management strategies, cardholders can leverage this feature to enhance their financial stability and avoid the pitfalls of high-interest credit card debt.

Regularly reviewing your EMI plan, understanding the terms, and utilizing available tools for budgeting and management can make a significant difference in maintaining financial health. Whether you are making a large purchase, facing an emergency expense, or simply seeking to manage your credit card balance more effectively, MER EMI provides a structured and manageable solution.

By following the comprehensive guide provided, you can navigate the complexities of MER EMI on HDFC credit cards with confidence and make informed decisions that align with your financial goals.